Breaking News

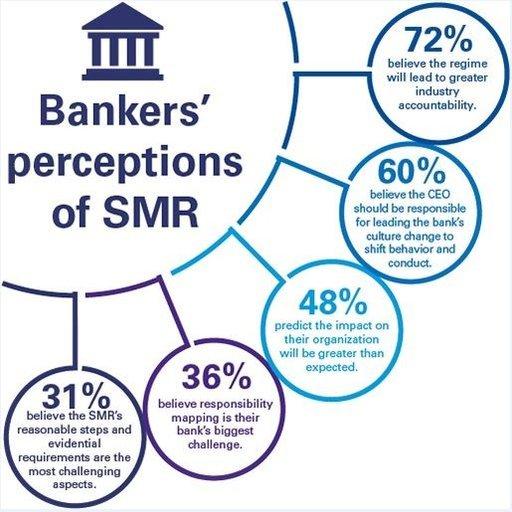

Two Expert Comments on SMR, Banks And Benchmarks

Chrisol Correia, head of international AML at LexisNexis® Risk Solutions comments on the lists of accountable individuals under the upcoming Senior Managers Regime (SMR)

“Recently, banks submitted their lists of staff that will be held responsible under the provisions of the Senior Managers Regime (SMR), creating additional pressure for financial crime compliance officers throughout the UK.”

“The SMR effectively holds compliance staff accountable to the same risks and responsibilities as the most senior management – but without the same level of reward. Last year our survey with the British Banking Association (BBA) found that more than half (54 per cent) of compliance professionals would choose another career path if given the opportunity in light of increased personal liabilities; unsurprising when there is risk of a custodial sentence. A skills shortage in this area would be highly disruptive due to the importance of the compliance officer role to not only individual banks, but the broader financial system.”

“The SMR and scheduled increase in criminal penalties growth in personal liabilities could make it more difficult for banks to recruit compliance officers. The global banking industry must ensure that compliance staff, who are under this increasing pressure to comply, are supported with accredited training. Compliance professionals also need to be equipped with effective resources to identify non-compliant and potentially illegal activity ahead of time, including the latest data and analytics tools, in order to mitigate the risk of becoming non-compliant and the serious consequences that follow.”

Haydn Lightfoot, Associate Partner at financial services consultancy Crossbridge, comments on the list of accountable people under the upcoming Senior Managers Regime (SMR).

“Many senior bankers will today be worried by the real risk they could face disciplinary action if the controls for which they are responsible fail to catch rogue colleagues breaking the law, and the regulator can subsequently prove these controls fell short of what should reasonably be expected. Whilst the onus is no longer on the individual manager to prove they took all reasonable preventative steps following the FCA’s removal of the presumed responsibility clause, bankers remain under pressure.

“Bankers could be given some reprieve, as it may be difficult for the regulator to prove beyond reasonable doubt that a top banker had not taken every reasonable step to prevent criminal activity. In order to create and maintain a minimum standard of compliance, the regulator should issue an industry-wide set of benchmarks which banks can be assessed against. This would provide real clarity and help the regulator rebuild public trust in our banks.”

- Smartstream: The Evolutionary Leap from Process Automation to Full Autonomy Read more

- How NOTO and Opus Advisory Group Are Unifying Fraud Prevention | NOTO, Opus Advisory Group | The Fintech Show #163 Read more

- AQMetrics’ Strategy for Unifying Data, Scaling for AI, and Building Trust Read more

- MPE 2026: G+D Netcetera on the Payment Security Stack Driving Higher Conversion and Lowering Fraud Read more

- InsurTech NY: Camunda on Smarter Workflows Read more

InsurTech NY: Camunda on Smarter Workflows

Share this post: Share on LinkedIn Share on X (Twitter) Share on Facebook Share on […]

InsurTech NY: Fair on Closing Coverage Gaps

Share this post: Share on LinkedIn Share on X (Twitter) Share on Facebook Share on […]

InsurTech NY: Teqfocus on Practical AI

Share this post: Share on LinkedIn Share on X (Twitter) Share on Facebook Share on […]

Moonfare Launches New AI-Focused Technology Strategy

Moonfare is pleased to announce the launch of a new AI-focused early and growth stage strategy designed to provide diversified exposure

Innovating Finance Together Summit Highlights the Power of Collaboration in a Fast-Changing Financial Landscape

Finastra’s inaugural Innovating Finance Together Summit, held in London, brought together more than 200 financial services professionals

Lydian Launches Co-Branded Visa Platinum Card, Turning Digital Assets Into Everyday Payments

Lydian, the leading digital assets payment infrastructure provider, is launching the Lydian Card, a co-branded Visa Platinum card

MENA Fintech Association Welcomes Facephi as a Member to Support Digital Identity and Secure Financial Onboarding Across the Region

Facephi joins MENA Fintech Association at a time when financial institutions across the Middle East are accelerating digital transformation

Smartstream: The Evolutionary Leap from Process Automation to Full Autonomy

Share this post: Share on LinkedIn Share on X (Twitter) Share on Facebook Share on […]

How NOTO and Opus Advisory Group Are Unifying Fraud Prevention | NOTO, Opus Advisory Group | The Fintech Show #163

Share this post: Share on LinkedIn Share on X (Twitter) Share on Facebook Share on […]

AQMetrics’ Strategy for Unifying Data, Scaling for AI, and Building Trust

Share this post: Share on LinkedIn Share on X (Twitter) Share on Facebook Share on […]

MPE 2026: G+D Netcetera on the Payment Security Stack Driving Higher Conversion and Lowering Fraud

Share this post: Share on LinkedIn Share on X (Twitter) Share on Facebook Share on […]

InsurTech NY: Camunda on Smarter Workflows

Share this post: Share on LinkedIn Share on X (Twitter) Share on Facebook Share on […]

Finastra: What Banks Must Do for 2026

Share this post: Share on LinkedIn Share on X (Twitter) Share on Facebook Share on […]

InsurTech NY: Fair on Closing Coverage Gaps

Share this post: Share on LinkedIn Share on X (Twitter) Share on Facebook Share on […]