Breaking News

Salt Edge report: State of open banking payments in Europe in 2021

Today we mark 2 years since PSD2 went, at least was supposed to, into full power across Europe and in the UK, on September 14, 2019. And as a tradition already, this year we’ve thoroughly analysed the performance of 2500 PSD2 APIs in 31 European countries, and the overall open banking journey they offer – both for a third party and an end-customer, and compiled the identified insights into a report.

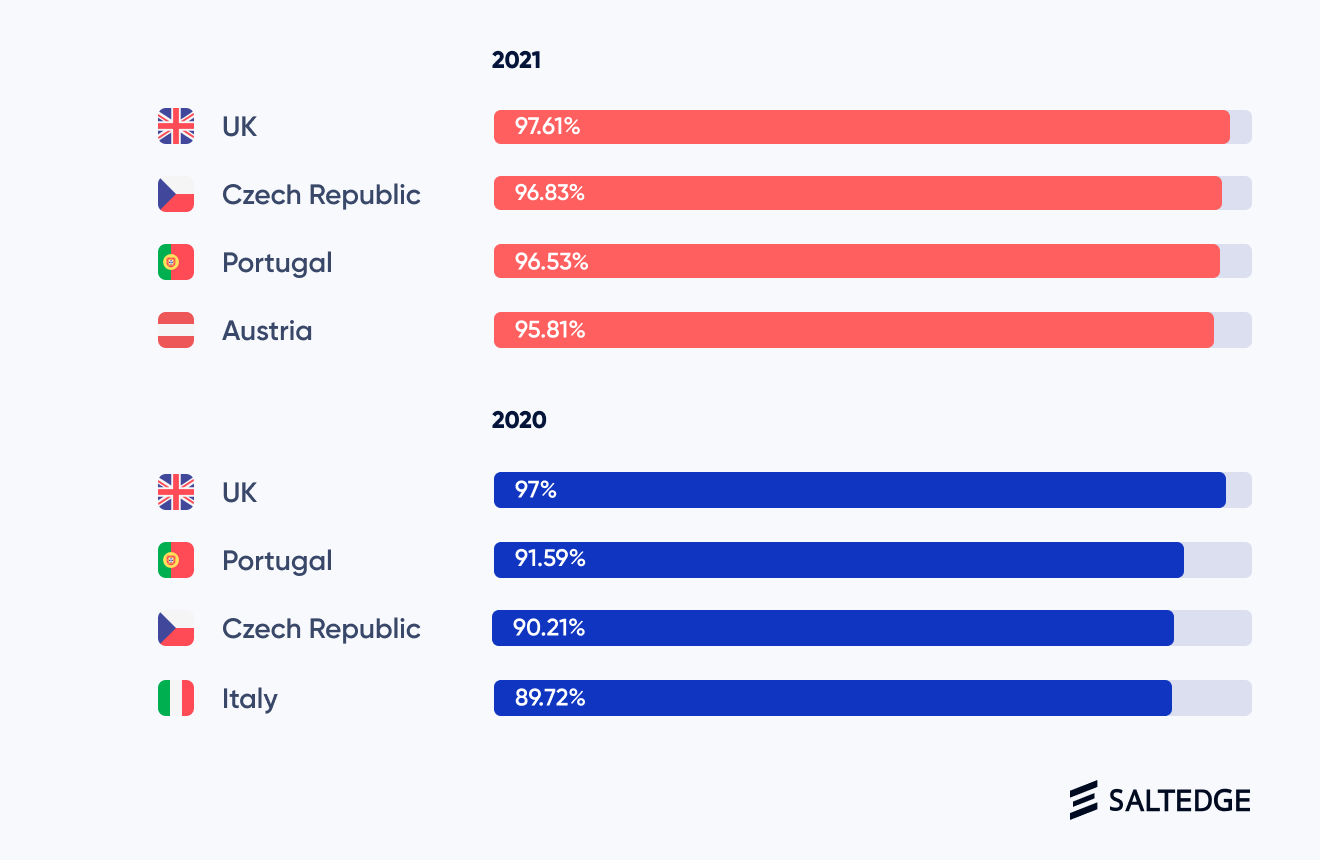

Noticing an increased appetite for open banking, especially for payment initiation services, Salt Edge has created a report that presents the current state of open banking in Europe, with a particular emphasis on payments. One might expect more things to have been achieved in these 2 years, yet we identified interesting dynamics compared to 2020. The APIs’ quality and availability have greatly improved, with top 10 EU countries having rates ranging from 97.61% to 91.12%. While last year the communication between TPPs and banks was mostly one-sided, this year the results have been calibrated and most API requests have been replied to.

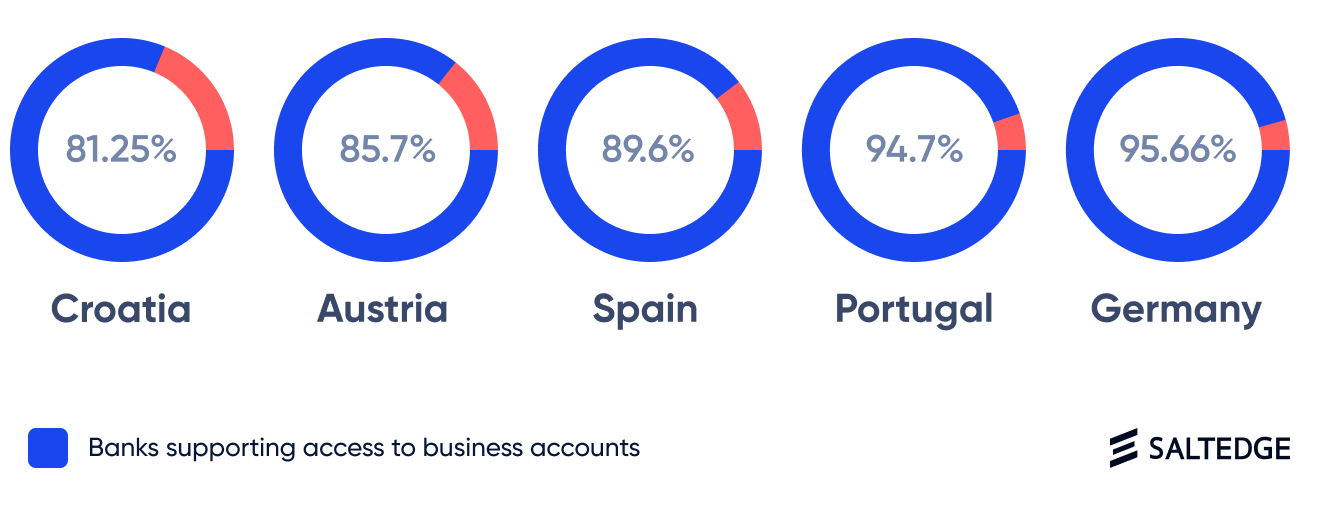

Out of the almost 2500 regulated APIs integrated by Salt Edge across Europe, 72% claim to be supporting access to business accounts. Germany, Portugal, Spain, Austria, and Croatia are the countries with the highest percentage of banks offering access to both personal and business accounts, creating an environment suitable for innovative services to emerge.

We were also pleasantly surprised to identify banks that offer access to more banking data than the one required by PSD2. For example, we identified banks in France, Greece, Denmark, the Netherlands, Slovakia, and other countries that have chosen to expand the data set made available through secure Open APIs including information about credit card transaction information, mortgage, savings, and investment accounts.

While in 2020 open banking payments APIs were almost not functioning, in 2021 banks offer an ecosystem, although not ideal, but one upon which new services can be built. To help customers in adopting open banking-powered payments, it is critical to ensure a smooth and intuitive user journey.

Yet, the current state of PSD2-enabled payments comes with various layers of complexity at each stage, to name a few: some banks request multiple redirects between the bank and third party (PIS) before a payment order is completed, PSU must go through other 6-8 additional pages which add unnecessary friction, a relatively small number of EU banks supporting mobile App-2-App redirection, banks’ PSD2 APIs not reflecting the actual payment status, banks having delays in consent management resulting in errors and user frustration. We’ve described in great detail these and other errors that we encountered at each step within the payment journeys in the report.

Download the report to discover more about the current reality of open banking in Europe, the identified differences between 2020 and 2021, the biggest obstacles in open banking payments, and much more.

Companies In This Post

- Sygnum Completes First Live AI-Agent Driven Digital Asset Transactions by a Regulated Swiss Bank Read more

- CMC Markets Launches Spectre Trading Account for Retail Clients Read more

- Ingenico and Arrive Partner to Power Seamless Payments for On‑Street Parking and Urban Transport Worldwide Read more

- Zurich Scales Agentic AI to Five Countries in 90 Days Cutting Manual Risk Processing Time by 80% Read more

- JCB and Wonder Advance Cashless Taxi Payments in Hong Kong Read more

Sygnum Completes First Live AI-Agent Driven Digital Asset Transactions by a Regulated Swiss Bank

Sygnum, a global digital asset banking group, today announced it has become the first Swiss regulated bank to use an AI agent to test live digital asset market transactions, with the client retaining custody, consent and control at every step. This is the latest initiative from AI@Sygnum which leads the development, integration and governance of agent-driven workflows across the group globally.

AS Colour Partners with Adyen to Complete the Global Customer Picture

Adyen, the global financial technology platform of choice for leading businesses, has announced its partnership with AS Colour, a designer and wholesaler of premium "blank" apparel, to streamline its global payment infrastructure and enhance the digital customer experience. Since partnering with Adyen in October 2025, AS Colour has consolidated multiple legacy payment providers into one global commerce platform, connecting its payments across all operating regions.

Nuvo and Avalara Launch AI Integration to Eliminate Tax Compliance Gaps and Accelerate B2B Customer Onboarding

Nuvo Technologies, the AI-native customer-to-cash platform, today announced an integration with Avalara, the agentic AI leader in global tax and compliance. The integration connects Nuvo’s AI-powered onboarding with Avalara’s exemption certificate management and real-time tax calculation capabilities—enabling B2B suppliers to handle credit applications and tax compliance in a single, unified experience. The result is a single workflow where suppliers can approve customers and ensure tax compliance at the same time.

Lumin Digital Unveils Lumin Solaire, an AI-Native Intelligence Layer Embedded In Its Compounding Growth Platform

Lumin Digital, the Compounding Growth Platform for banks and credit unions, today unveiled Lumin Solaire, an AI-native intelligence layer embedded across its platform. The announcement was made at Lumination, the company’s annual client conference, where Lumin is showcasing its platform strategy and product roadmap.

Sturgis Bank Partners with MANTL to Transform Business and Retail Account Opening Across All Banking Channel

Alkami Technology, Inc. (Nasdaq: ALKT) ("Alkami"), a digital sales and service platform provider for financial institutions in the U.S., today announced a new partnership between MANTL, an Alkami solution team and leading provider of loan and deposit account opening technology, and Sturgis Bank, a community bank serving Michigan through 16 branches, to transform its account opening experience for business and retail customers. Through this partnership, Sturgis Bank will modernize onboarding across all physical and digital banking channels, reinforcing its commitment to delivering a seamless, efficient, and customer-centric experience while expanding accessibility and accelerating digital growth.

Digital Assets Clearing Center Secures US$10 Million Funding for International Market Infrastructure

Digital Asset Clearing Center (DACC.HK), a next-generation financial market infrastructure for the tokenized economy, today announced US$10 million in funding from strategic partners including Conflux, Transaction Technologies Limited (“TTL”) and Global InfoTech. Traditional bank transfers continue to dominate the US$214 trillion cross-border payments market, but tokenized finance offers an alternative to slow settlement cycles, high transaction costs, fragmented data systems and regulatory barriers. Digital Asset Clearing Service offers seamless connections to the world's leading payment systems including Cross-Border Interbank Payment System (CIPS), blockchain networks and compliance infrastructure delivering end-to-end Clearing-as-a-Service (CaaS) for financial institutions.

Apex Group Provides Transfer Agency Services in Support of the Launch of Fidelity International’s First Tokenised Product

Apex Group Ltd (“Apex Group”) a global financial services provider with over $3.5 trillion in assets serviced, today announced that it is providing transfer agency services to Fidelity International in support of the launch of its first tokenised product, which offers institutional and professional investors 24/7 liquidity. The capabilities are designed for on‑chain markets and real‑time processing environments.

Sygnum Completes First Live AI-Agent Driven Digital Asset Transactions by a Regulated Swiss Bank

Sygnum, a global digital asset banking group, today announced it has become the first Swiss regulated bank to use an AI agent to test live digital asset market transactions, with the client retaining custody, consent and control at every step. This is the latest initiative from AI@Sygnum which leads the development, integration and governance of agent-driven workflows across the group globally.

CMC Markets Launches Spectre Trading Account for Retail Clients

CMC Markets (“CMC”), a FTSE 250 company and global leader in multi-asset online trading and investing, has launched Spectre for retail clients, following strong demand after the product was initially introduced for professional traders.

Ingenico and Arrive Partner to Power Seamless Payments for On‑Street Parking and Urban Transport Worldwide

Ingenico, a global leader in payment acceptance solutions, and Arrive, a leading global mobility platform, today announced a strategic partnership to deliver reliable, seamless payment experiences for on-street parking and transport ticket vending machines across more than 30 countries worldwide.

Zurich Scales Agentic AI to Five Countries in 90 Days Cutting Manual Risk Processing Time by 80%

Zurich Insurance has completed a breakthrough 90‑day deployment of Cytora’s agentic AI‑powered risk digitization platform across five countries. The programme will now scale to more than 20 markets over 16 months.

JCB and Wonder Advance Cashless Taxi Payments in Hong Kong

JCB International Co., Ltd, the international operations subsidiary of JCB Co., Ltd, Japan’s only international payment brand, and Wonder Ventures Limited, a leading payments and fintech platform in the Asia Pacific, announced that JCB Cards are now accepted on Wonder Taxi in Hong Kong.

AS Colour Partners with Adyen to Complete the Global Customer Picture

Adyen, the global financial technology platform of choice for leading businesses, has announced its partnership with AS Colour, a designer and wholesaler of premium "blank" apparel, to streamline its global payment infrastructure and enhance the digital customer experience. Since partnering with Adyen in October 2025, AS Colour has consolidated multiple legacy payment providers into one global commerce platform, connecting its payments across all operating regions.

Nuvo and Avalara Launch AI Integration to Eliminate Tax Compliance Gaps and Accelerate B2B Customer Onboarding

Nuvo Technologies, the AI-native customer-to-cash platform, today announced an integration with Avalara, the agentic AI leader in global tax and compliance. The integration connects Nuvo’s AI-powered onboarding with Avalara’s exemption certificate management and real-time tax calculation capabilities—enabling B2B suppliers to handle credit applications and tax compliance in a single, unified experience. The result is a single workflow where suppliers can approve customers and ensure tax compliance at the same time.